RBA's latest forecasts are grim. Here are 5 reasons why

- Written by Isaac Gross, Lecturer in Economics, Monash University

After lifting interest rates for a record nine times in a row, and flagging more raises still to come, the Reserve Bank of Australia’s latest set of forecasts make for grim reading.

The forecasts are part of the central bank’s quarterly Statement on Monetary Policy[1], its main communication (aside from interest rates) on how it sees the economy faring over coming few years.

The bad news is the bank tips economic growth to slow, inflation to remain high, spending to stagnate, unemployment to increase, and real wages to fall further.

The good news is that it could be wrong.

1. Growth is expected to slow

The central bank expects Australia’s economy to slow this year due to rising interest rates, higher cost of living, and declining house prices.

It tips GDP growth for 2022 will be 2.75% (the Australian Bureau of Statistics won’t publish this data until March), and 1.5% over 2023 and 2024.

This compares to the RBA’s expectation three months ago[2] of 3% growth in 2022, but is the same as the previous prediction for this year and the next.

RBA GDP growth forecasts

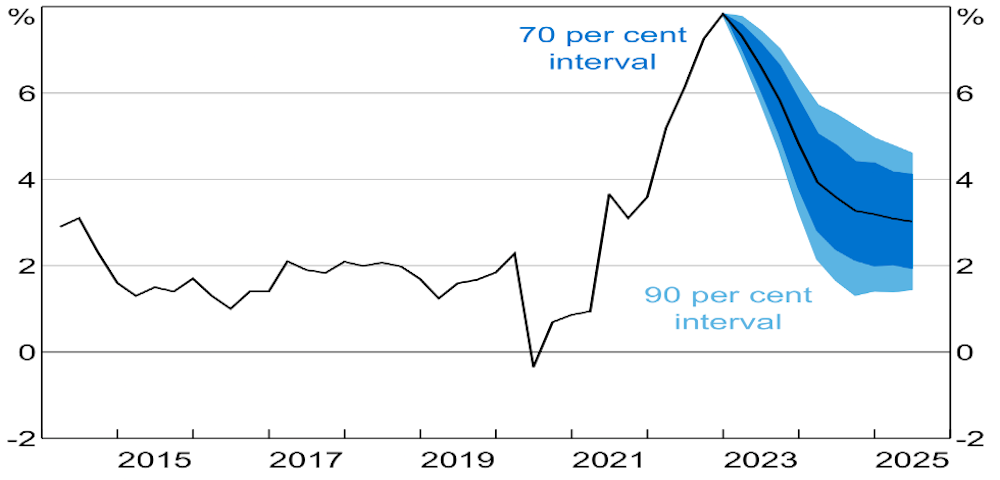

2. Inflation will remain high

The bank says inflation, which hit 7.8% in 2022, is likely to have peaked and will stay high for several months, but should decline to 4.5% by the end of 2023.

By mid-2025 the bank expects inflation to have fallen to back to 3% – the top end of its inflation target range of 2-3%.

However, the pace of this fall depends on wages and prices. The bank acknowledges inflation could fall more quickly or more slowly.

RBA headline inflation forecasts

Confidence intervals reflect RBA forecasting errors since 1993. Year-end forecasts.

RBA[4]

Confidence intervals reflect RBA forecasting errors since 1993. Year-end forecasts.

RBA[4]

Australian consumer price inflation has been high due to factors including global supply-chain disruptions caused by the pandemic, Russia’s invasion of Ukraine, strong domestic demand, a tight labour market, and capacity constraints.

The bank expects rising energy prices to continue to drive inflation but expects this to be offset by the government’s Energy Price Relief Plan, which caps gas and coal prices, will subsidise household and business bills.

Read more: Will price caps on gas bring power prices down? An expert isn't so sure[5]

Price increases for goods such as food and furniture are expected to moderate. But the cost of services will continue to rise, due to wage growth.

This is the main reason the RBA has flagged more interest rate hikes this year. It is determined to get inflation back to its target band, and will keep increasing borrowing rates until it is sure this goal will be achieved.

3. Consumer spending will stagnate

The bank’s statement says higher consumer prices, higher interest payments and lower household net wealth are expected to curb consumer spending in 2023.

But it says spending should improve once interest rate rises stop, household wealth recovers and disposable incomes are boosted by tax cuts.

The household saving ratio (which doubled during the pandemic) is expected to fall below the pre-pandemic norm of 5% before clibing back to pre-pandemic levels in 2024.

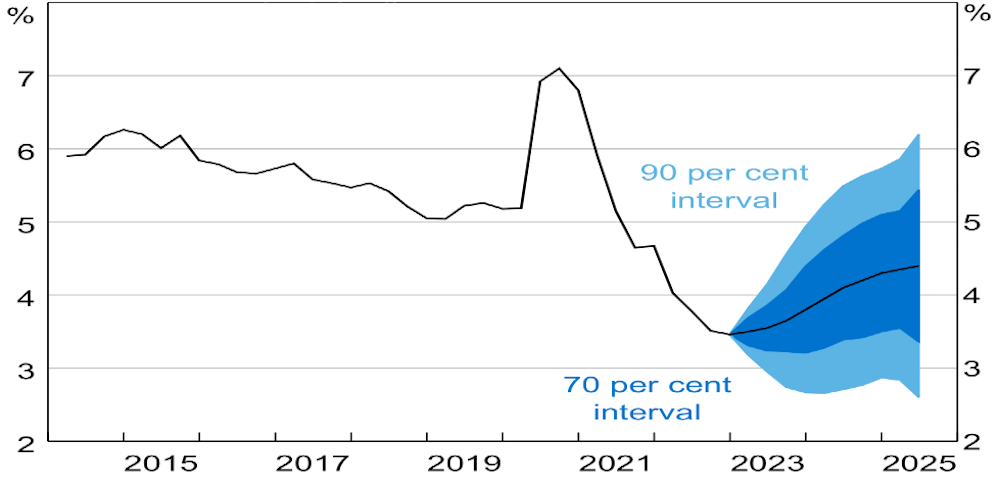

4. Unemployment will climb

The bank expects the unemployment rate to remain at about 3.5% until mid-2023, and then to climb to 4.5% as demand for labour moderates.

4.5% remains well below where it has been for most of the past half century.

RBA unemployment rate forecasts

Confidence intervals reflect RBA forecasting errors since 1993.

RBA[6]

Confidence intervals reflect RBA forecasting errors since 1993.

RBA[6]

Jobs growth is forecast to slow from 4.8% in 2022 to about 1% by mid-2024.

Despite this, the participation rate in the labour force is not expected to fall, due to structural trends such as higher female and older worker participation.

5. Real wages will fall

The RBA’s forecast for wages growth is now higher than three months ago, due to a tight labour market, higher staff turnover, higher inflation outcomes and Fair Work Commission wage decisions.

It tips the Wage Price Index, which hasn’t been above 4%[7] in a decade, to hit 4.25%.

Given the inflation rate, however, this won’t be enough wages growth to stop real wages from continuing to fall.

The wage price index is tipped to fall back to 3.75% in mid-2025 as the demand for labour subsides and unemployment climbs.

Uncertainty remains high

These forecasts make for grim reading. But they could all be quite wrong. As the saying goes, it’s tough to make predictions, especially about the future.

Huge uncertainties hang over the global economy, including the war in Ukraine, the emergence of new COVID variants, and the unique challenges of recovering from the pandemic.

That means all these forecasts could be – and likely will be – wrong in one dimension or another.

Even the governor’s very clear message[8] that there will be more interest rate rises this year could change if the prevailing circumstances do too. Time will tell.

Read more: Higher interest rates, falling home prices and real wages, but no recession: top economists' forecasts for 2023[9]

References

- ^ Statement on Monetary Policy (www.rba.gov.au)

- ^ three months ago (www.rba.gov.au)

- ^ RBA (www.rba.gov.au)

- ^ RBA (www.rba.gov.au)

- ^ Will price caps on gas bring power prices down? An expert isn't so sure (theconversation.com)

- ^ RBA (www.rba.gov.au)

- ^ hasn’t been above 4% (www.abs.gov.au)

- ^ very clear message (theconversation.com)

- ^ Higher interest rates, falling home prices and real wages, but no recession: top economists' forecasts for 2023 (theconversation.com)

Authors: Isaac Gross, Lecturer in Economics, Monash University

Read more https://theconversation.com/rbas-latest-forecasts-are-grim-here-are-5-reasons-why-199509