Why does the RBA keep hiking interest rates? It's scared it can't contain inflation

- Written by Peter Martin, Visiting Fellow, Crawford School of Public Policy, Australian National University

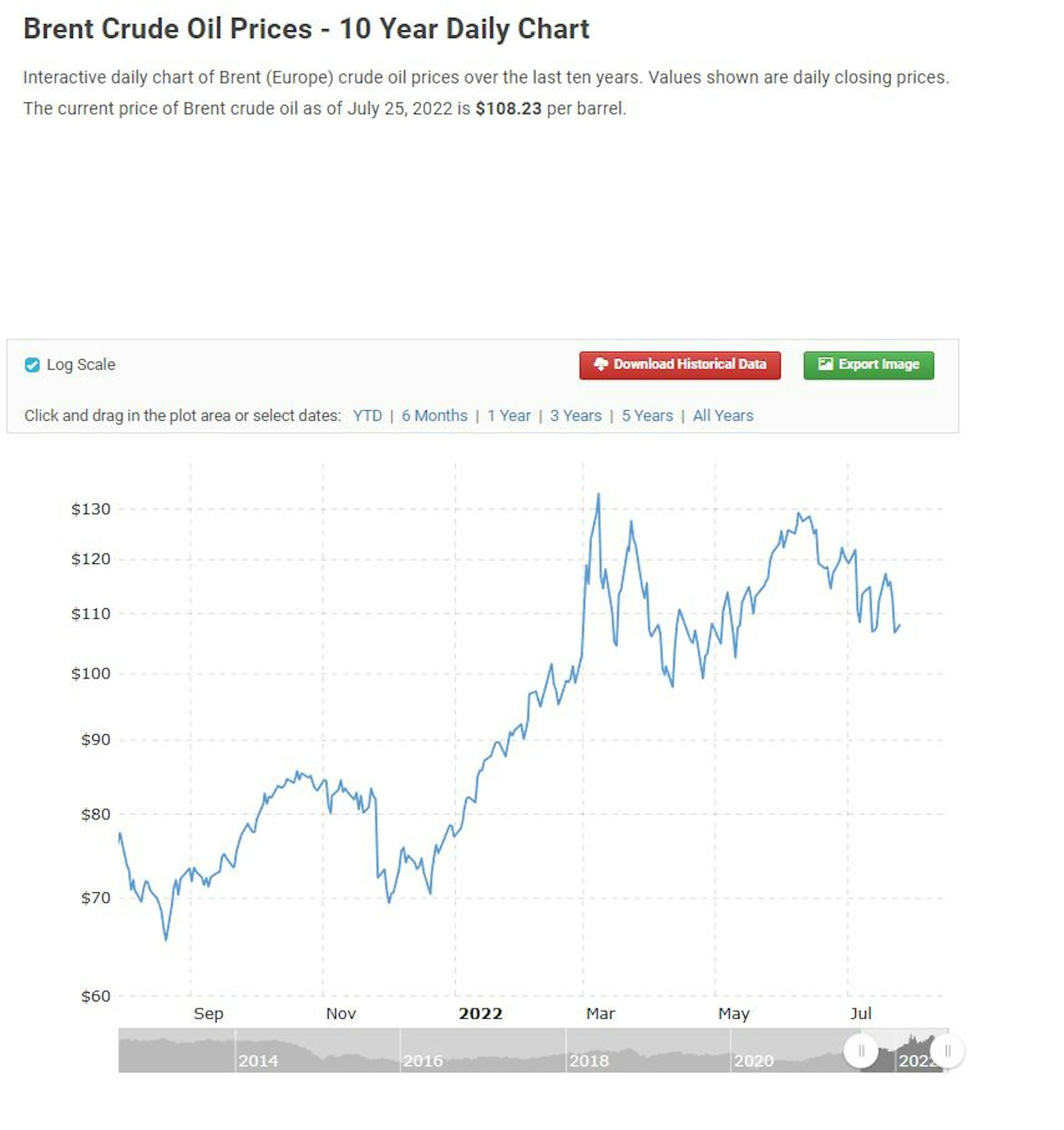

There are signs inflation pressures are easing. Oil prices are down almost 20% on their peak in March. They’ve been falling consistently for a month[1].

The average capital city unleaded price is down from A$2.11 per litre in early July to a more bearable $1.74[2].

The money market is pricing in much lower inflation than we presently have over the next one to four years[3], and consumers’ inflation expectations (although still high at 6.3%) eased off a bit[4] between June and July.

So why did the Reserve Bank just hike its cash rate by an outsized 0.50 percentage points for the third consecutive month[5], taking it to 1.85%?

Partly because it knows what is to come.

Higher inflation in store

The 6.1% inflation figure released last week was for the year leading to the quarter that ended in June[6]. Since then, in July, we’ve been hit by massive electricity price increases, some as high as 19%[7], and gas prices that have manufacturers screaming[8].

The monthly inflation gauge compiled by the Melbourne Institute (the Bureau of Statistics hasn’t yet gone monthly) kicked up 2.1%[9] in July, the biggest monthly jump in two decades.

And there’s something else.

The Reserve Bank’s deepest fear might be that it can’t contain inflation, and that its apparent success over three decades has owed a lot to luck.

Reserve banks blessed by luck

Inflation fell to low levels throughout the world around the world at about the time it fell to low levels in Australia. From the mid 1990s, inflation fell to 2-3% in the US, the UK, Canada[10] and just about every other Western nation, as China deluged the world with low-priced goods and companies began offshoring.

It got to the point where almost as many prices were falling as rising.

The US economic historian Adam Tooze says it’s reasonable to ask whether we had inflation at all from the mid 1990s onwards.

The Bank for International Settlements defines inflation as a “largely synchronous increase in the prices of goods and services[11]” – a situation where prices broadly climb together.

Little real inflation for 30 years

It needs to be largely synchronous to qualify as inflation because otherwise the amount a dollar can buy isn’t clearly changing – any such effect is overwhelmed by changes in the mix[12] of goods and services a dollar can buy.

It is only when prices start to move together, as they are now, that inflation gets normalised and becomes entrenched.

Twenty years ago, in June 2002, by my count 20 of the 87 types of items that made up the consumer price index fell in price. Ten years ago, 32 fell in price.

By economist Saul Eslake’s count, this June only 15 of what are now 90 expenditure classes fell in price – what appears to be the lowest number in decades.

Suddenly, price rises are synchronised

It means the Reserve Bank is having to deal with broad-based inflation of a kind it hasn’t faced since it began targeting inflation[13] in the early 1990s.

Just about the only tool it has to do it – higher interest rates – makes people poorer.

Higher interest rates work in other ways as well.

they increase the reward for saving, diverting some money from spending

they make it harder to borrow, diverting more money from spending

and they push up the exchange rate, making imported goods cheaper – or they would have, were other central banks not also pushing up their rates, meaning the Australian dollar is no higher than it was when the bank began pushing up rates in May.

But their chief effect is impoverishing variable mortgage holders, to the tune of hundreds of dollars a month[14].

The more variable mortgage rates go up (Tuesday’s hike will push up the ANZ standard rate from 4.24% to 4.74%) the less mortgage holders have to spend on other things, and the less they will add to price pressure.

That’s the idea. And it is disingenuous to pretend otherwise.

Mortgage buffers are scant protection

In a speech last month Reserve Bank Deputy Governor Michele Bullock said households in aggregate were “well positioned[15]”.

They had saved $260 billion since the start of the pandemic, much of which had gone into redraw facilities and offset and deposit accounts.

Around half were almost two years ahead on mortgage payments, or more. They had “large buffers”.

But, as University of Newcastle economist Bill Mitchell points out, by the bank’s own logic, this just means it will have to squeeze them harder[16].

Read more: The RBA's rate hikes will add hundreds to monthly mortgage payments[17]

It wants Australians to spend less and, if they use their buffers to keep spending as they have, it will have to either give up, or push rates higher until they do.

RBA Governor Philip Lowe says he is navigating a “narrow path[18]” to curb inflation without too much pain. He can’t be certain he knows the way.

References

- ^ for a month (images.theconversation.com)

- ^ $1.74 (aip.com.au)

- ^ one to four years (www.datawrapper.de)

- ^ eased off a bit (melbourneinstitute.unimelb.edu.au)

- ^ third consecutive month (www.rba.gov.au)

- ^ June (theconversation.com)

- ^ some as high as 19% (www.smh.com.au)

- ^ screaming (www.afr.com)

- ^ 2.1% (www.afr.com)

- ^ Canada (www.inflationtool.com)

- ^ largely synchronous increase in the prices of goods and services (cdn.theconversation.com)

- ^ mix (adamtooze.com)

- ^ began targeting inflation (theconversation.com)

- ^ hundreds of dollars a month (theconversation.com)

- ^ well positioned (www.rba.gov.au)

- ^ squeeze them harder (bilbo.economicoutlook.net)

- ^ The RBA's rate hikes will add hundreds to monthly mortgage payments (theconversation.com)

- ^ narrow path (www.rba.gov.au)

Authors: Peter Martin, Visiting Fellow, Crawford School of Public Policy, Australian National University

{kind=link}